Spanish brick sector closes 2024 with sustained growth and calls for urgent measures to ensure housing supply

The Spanish Association of Baked Clay Brick and Roof Tile Manufacturers (Hispalyt) presented at a press conference on 28 May 2025 the balance sheet of the structural ceramics sector for 2024, as well as the main demands to face the challenges of the future in terms of housing, energy, labour and regulations.

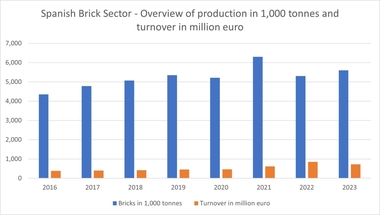

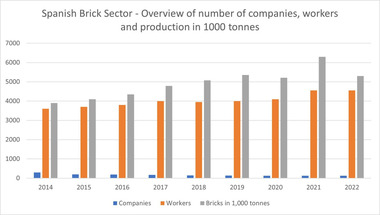

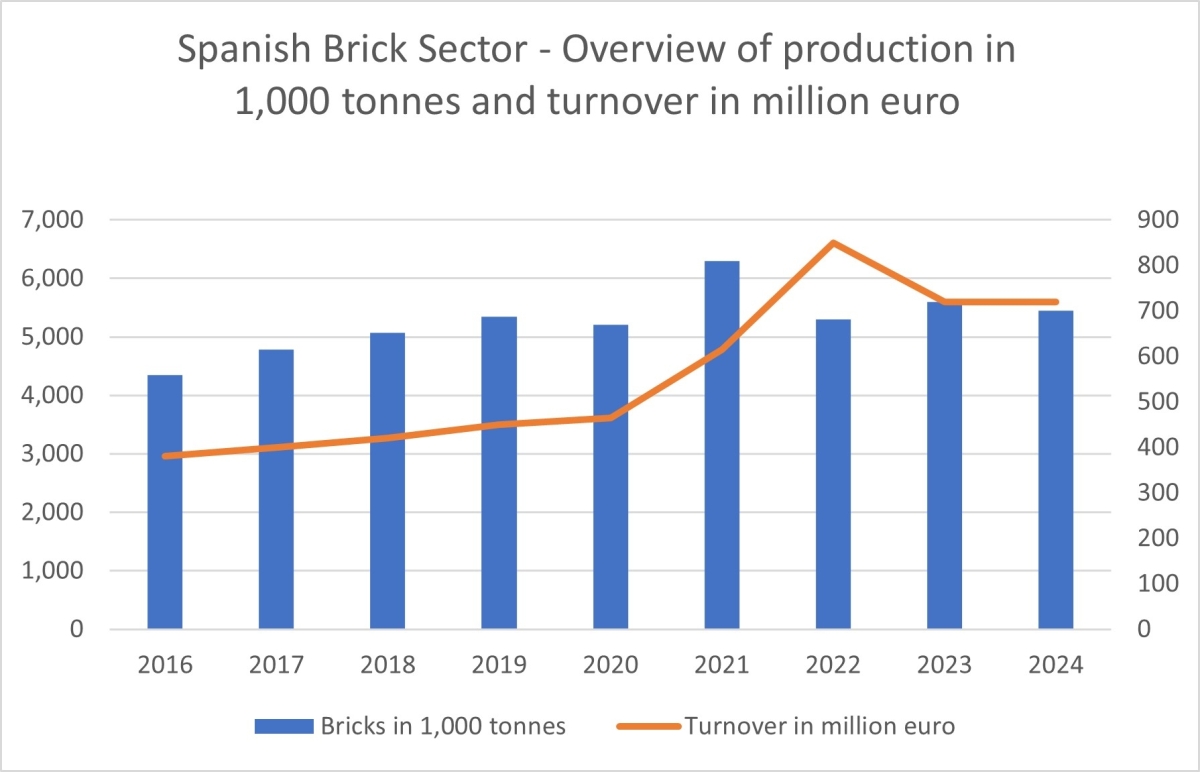

The bricks and tiles sector closed the last financial year with 130 active companies, a production of 5.45 million tonnes and a turnover of 719 million euros. Despite the slight drop of 0.1 percent in turnover compared to 2023, it consolidated a growth of 105 percent compared to 2014. Employment also grew by 1.8 percent reaching 4,877 workers, with an accumulated increase of 35 percent over the last decade.

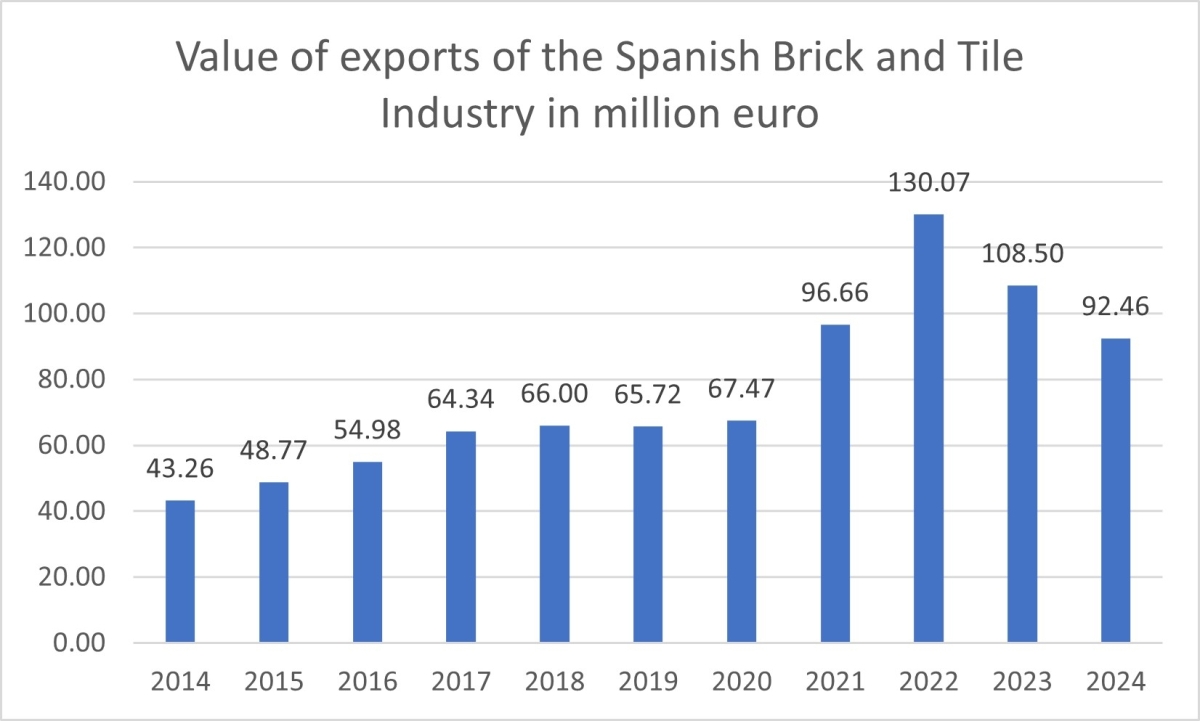

On the other hand, exports in the sector reached 92 million euros, 90 percent more than a decade ago, consolidating Spain as the second European exporter and fourth in global volume.

The vice-president of Hispalyt, Francisco Rodríguez, assessed these figures positively, assuring that the sector faces the future with optimism. “In view of these figures, we can say that we have a consolidated, efficient sector that generates economic and social value. Business stability, accumulated growth in production, business and employment position the sector as a benchmark of resilience, competitiveness and continuous progress. We will continue to work along these lines to face the future with guarantees”, he declared.

Housing shortage in Spain

Francisco Rodríguez analysed the data on housing construction and the current problems in this regard. The forecasts for the construction sector show moderately optimistic growth, with estimates of up to 4 percent for 2025, and 2.7 percent for 2026. However, he pointed out, ‘these figures are insufficient to address the country’s profound housing deficit, which is estimated at around 600,000 units between 2022 and 2025’.

Rodriguez warned that this imbalance between supply and demand is not only not being corrected, but threatens to worsen if urgent action is not taken. The sector has precedents that demonstrate its capacity. In previous periods, he said, ‘up to 700,000 homes were built annually. At present, however, annual production barely reaches 200,000-250,000 homes, far below real needs, which could lead to an accumulated deficit of between 700,000 and 750,000 homes in the coming years’.

The vice-president of Hispalyt explained that the main obstacle identified is the scarcity of developable land and the slowness of the procedures. The process of land transformation is excessively slow, as Rodriguez explained, it takes 10 years to change from rural land to developable land, 3 years to execute the urbanisation projects, 1 year to process licences and 2 years for construction. This cycle has prevented the generation of new land for development at the pace required. Furthermore, he noted as worrying the almost total disappearance of public housing since then.

In this context, reference was also made to the breakdown of the costs that influence the total price of housing. He alluded to a study carried out by the Association of Real Estate Developers of Madrid, Asociación Promotores Inmobiliarios de Madrid (Asprima), in which it can be seen that around 57 percent of the final price of housing corresponds to land and taxes, with only 16 percent being construction costs, of which less than 10 percent corresponds to materials.

This data is relevant because, as the head of Hispalyt stated, ‘the widespread perception that the increase in the cost of housing is mainly due to the increase in the price of materials is completely dismantled, because in reality, their weight in the total cost is relatively limited’.

‘Our sector is part of the solution, not part of the problem,’ said Francisco Rodríguez, adding that, in view of this situation, Hispalyt proposes a clear roadmap, ‘freeing up more land for development, speeding up urban planning procedures and unblocking the Land Law. Only in this way will it be possible to respond to the growing demand for housing and prevent the structural deficit from continuing to increase’.